Beyond mega-deals: who is really shaping Africa's startup ecosystem?

Executive Summary

▾- This is the first article in a series co-authored by Dama & Co and The Uplift, aimed at unpacking the structural dynamics of venture capital across African ecosystems. The French version can be found here.

- This article analyses Africa's VC ecosystem as a structurally uneven market, where $4.1B raised in 2025 masks significant concentration across a small number of hubs.

- Capital flows remain heavily clustered in Nigeria, Egypt, Kenya, and South Africa, while most of the continent operates with limited access to growth-stage funding despite sustained entrepreneurial activity.

- A comparative lens on Kenya, Senegal, and Angola highlights three distinct trajectories: from mature ecosystems to structurally underfunded environments.

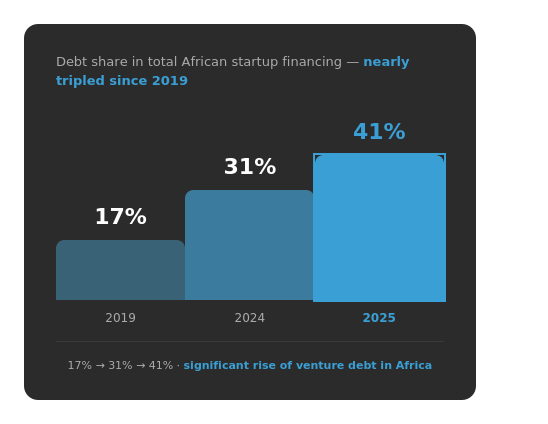

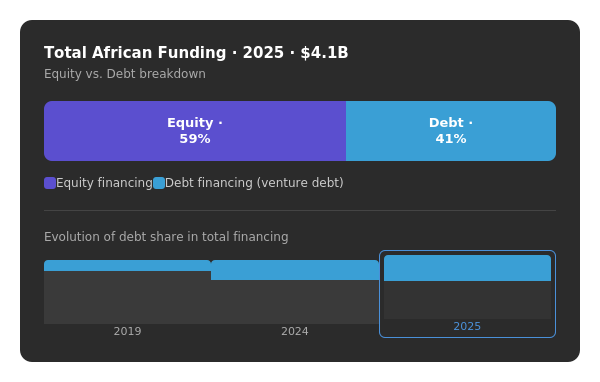

- The growing share of debt (41% in 2025) signals a broader shift in financing structures and risk appetite.

- Africa's startup ecosystem is not a single market, but a multi-speed system where access to capital remains unevenly distributed.

Introduction

It is no secret that Africa's startup ecosystem continues to capture attention, often through headline-grabbing funding rounds that reinforce the idea that this is a market not to be underestimated.

In 2025, according to consolidated data from Partech, African startups raised approximately $4.1 billion, combining both equity and debt financing. This momentum is further illustrated by several major transactions: Egyptian proptech company Nawy raised $52 million, while players such as Moniepoint in Nigeria and MNT-Halan in Egypt crossed the symbolic $100 million mark.

At first glance, these figures suggest a fast-growing, increasingly sophisticated ecosystem that is attracting investors. Yet behind these strong performances lies a more nuanced and unequal reality.

I. A concentrated growth: the illusion of a homogeneous market.

A closer look at the data reveals a defining feature of venture capital in Africa: its extreme concentration.

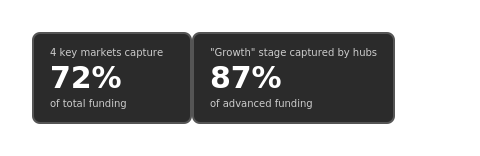

The majority of funding is concentrated in four key markets (Nigeria, Egypt, Kenya, and South Africa) which together account for approximately 72% of total funding and more than 80% of equity investments. This concentration is even more pronounced at later stages, with nearly 87% of growth-stage funding absorbed by these markets.

An extreme concentration.

By contrast, the rest of the continent (over forty countries) represents only around 15% of total funding volumes, despite accounting for nearly 27% of all transactions.

"Activity exists, but access to transformative capital remains limited."

In other words, Africa's venture capital landscape is far from homogeneous. While widely publicized mega-deals reinforce the perception of a unified and thriving market, access to capital remains deeply uneven across the continent.

This raises a fundamental question: is Africa's startup ecosystem truly unified, or is it a multi-speed market?

II. A comparative perspective: three trajectories, three realities.

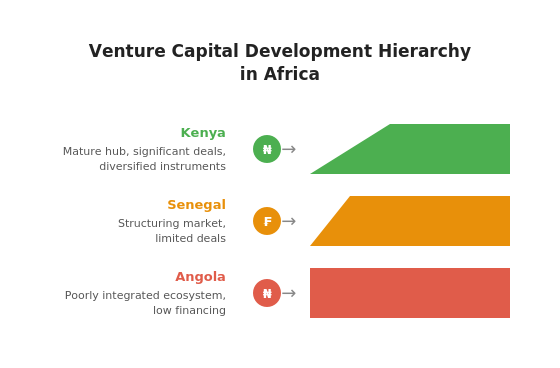

To illustrate this asymmetry, a comparison of three technology investment markets — Kenya, Senegal, and Angola — is particularly revealing.

a. Kenya: one of the continent's most mature hubs.

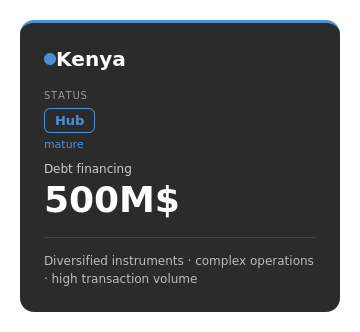

Kenya stands out as one of the continent's most mature hubs. It combines a high volume of transactions with a strong ability to attract capital, particularly through diversified instruments such as debt. In 2025 alone, the country mobilized nearly $500 million in debt financing, reflecting an ecosystem capable of absorbing significant capital and structuring complex deals.

Kenya, a mature hub.

b. Senegal: a market in transition.

Senegal, by contrast, represents a market in transition. Activity is real and growing, with an increasing number of transactions and improved visibility among investors. However, funding volumes remain highly dependent on a limited number of deals. In 2025, Senegal mobilized $139 million in debt across just two transactions, compared to $84 million in equity across ten deals. Scaling remains constrained.

A market in transition.

c. Angola: a case of structural disconnect.

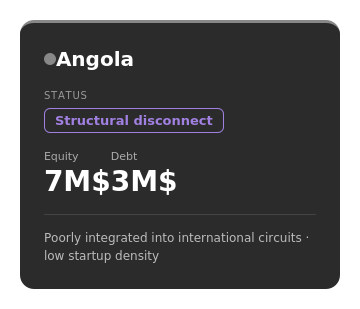

Angola, finally, illustrates a case of structural disconnect. Despite its economic weight driven by natural resources, the country attracted only around $10 million in funding in 2025 ($7 million in equity and $3 million in debt). This level is extremely low relative to its potential and reflects an ecosystem that remains weakly integrated into international venture capital networks.

A structural disconnect.

This comparison highlights a key reality: Africa's venture capital ecosystem does not evolve linearly, but rather across multiple speeds.

III. The mega-deal illusion.

This concentration is amplified by a media phenomenon: the overrepresentation of mega-deals.

Funding rounds above $100 million, while relatively rare, shape the perception of the market. They project the image of an ecosystem in rapid expansion, capable of absorbing large volumes of capital.

However, this narrative obscures a critical reality: the majority of African startups operate in an environment where capital remains scarce and fragmented.

The contrast between deal volume and investment value illustrates this clearly: roughly a quarter of transactions take place outside major hubs, yet they account for only a marginal share of total capital deployed.

"The ecosystem is growing, but access to capital remains deeply unequal."

IV. Francophone vs. Anglophone: a more nuanced picture.

Another key finding challenges a common assumption: regional dynamics do not always align with prevailing perceptions. Contrary to the widespread belief that anglophone markets dominate the entire continent, the data tells a more complex story. According to Partech data, in secondary markets, francophone countries captured 68% of equity investment volumes and 64% of transactions in 2025 (6). This reveals a dual reality: Anglophone hubs continue to dominate the largest funding rounds and advanced stages (growth/late-stage). Francophone markets, however, are playing a leading role in driving capital distribution at earlier stages. This has resulted in an implicit specialization: major hubs capture the large-scale growth capital, while secondary markets generate the volume and flow of early-stage transactions. However, this dynamic raises a critical structural question: Can startups operating in these secondary markets access the same levels of financing, or must they inevitably connect to dominant hubs to scale?

V. A shifting landscape: the rise of debt financing.

Beyond geographic dynamics, Africa's venture capital ecosystem is undergoing a more discreet but significant transformation: the rise of debt financing.

In 2025, nearly 41% of total funding came from debt, up from 31% in 2024 and 17% in 2019, marking a substantial increase in the use of venture debt across the continent.

This trend reflects a deeper shift in the market. On one hand, it signals increasing maturity, with startups capable of leveraging more complex financial instruments beyond pure equity. On the other, it reflects growing caution among equity investors in a global context of tighter funding conditions.

This evolution is not without implications. It introduces new challenges, particularly in terms of legal structuring, guarantees, and financial governance.

VI. Beyond the numbers: who actually accesses capital?

These observations raise several fundamental questions:

- Do the headline funding rounds truly reflect the state of investment in Africa?

- How do linguistic, geographic, and institutional dynamics shape access to capital?

- More broadly, which founder profiles are able to raise funding? And why?

These questions call for moving beyond a purely quantitative reading of the market to examine the structural mechanisms that underpin access to capital.

VII. A series to decode Africa's venture capital dynamics.

It is within this context that Dama & Co and The Uplift have partnered to launch this article series, aimed at unpacking trends, analyzing data, and shedding light for investors, entrepreneurs, and other ecosystem actors on the inner workings of Africa's entrepreneurial landscape.

The upcoming pieces will explore:

- Regional disparities and capital concentration dynamics

- The impact of linguistic dynamics on access to funding

- Gender-based inequalities in access to capital

- The role of individual trajectories, between local talent and diaspora

- The often underestimated influence of grants in shaping ecosystems

Scope of analysis: For the purposes of this series, a startup will be considered African if it primarily operates on the African continent, or if its operational team is predominantly based on the continent.

To stay informed about upcoming articles in this series, sign up here.

Conclusion: understanding rather than observing.

In a context where funding announcements dominate the narrative, the ambition of this series is different: to understand the deeper mechanisms that shape access to capital in Africa.

Because beyond the amounts raised, it is the underlying (often invisible) legal, economic, and structural dynamics that ultimately determine the trajectory of African entrepreneurial ecosystems.

"Africa's startup ecosystem is often described as 'growing.' But who is that growth really benefiting? And if not everyone, why?"

This is what this series aims to explore.

Sources

- Nawy, the largest proptech in Africa, raises a $52M Series A to take on MENA, Partech – May 12th, 2025: partechpartners.com

- Moniepoint has raised US$110 million to power the dreams of millions of Africans everywhere, Moniepoint – October 29th, 2024: moniepoint.com

- Africa Tech Venture Capital, 2025 Partech Partners Report: partechpartners.com

- African Private Equity and Venture Capital Association, Venture Capital Activity in Africa, H1 2025 in Review.

- Africa The Big Deal database

1 comment

AU-DELÀ DES MÉGA-DEALS : QUI FAÇONNE RÉELLEMENT L'ÉCOSYSTÈME AFRICAIN ? — Dama Advisory

Ping : AU-DELÀ DES MÉGA-DEALS : QUI FAÇONNE RÉELLEMENT L’ÉCOSYSTÈME AFRICAIN ? – Dama Advisory